Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

This month’s introduction is a little longer than usual. Whoops.

I’ll take the extra few words to set the stage in light of our current economic instability and market forces before jumping into the stats. For those wanting to just jump into the numbers, scroll to the next section… but then scroll back to the introduction because I make some good points 😊

INTRODUCTION

Recently I was reading an article about the local real estate market uncertainty and came across a line that I think applies to the March stats. The line was:

“While today’s tariff tensions and political uncertainty present a very different kind of challenge, they share one key trait: hesitation. In moments like this, the market doesn’t collapse—it pauses. And when clarity returns, buyers and sellers tend to come back with purpose. ” (Source: REM)

The stats speak for themselves. We have a buyer’s market in many segments and areas… but buyers have currently taken a pause. Understandably this stems from the uncertainty of how the real estate market will respond to the actions of others outside of our sovereign borders.

BUT the conditions are currently the best they have ever been for buyers in recent memory. Quoting another market intelligence source I recently read – “A Market Made for Buyers is Missing Buyers” (Source: Greater Vancouver Realtors)

Last month I wrote “Is it possible to Time The Real Estate Market” – the short answer is no. The right time to make a purchase in the real estate market is when you can afford it. Take a look at my article here which poses key questions for anyone considering a real estate purchase – in any market.

If you have questions, give me a call and we can review your specific situation and real estate ambitions.

On to the numbers!

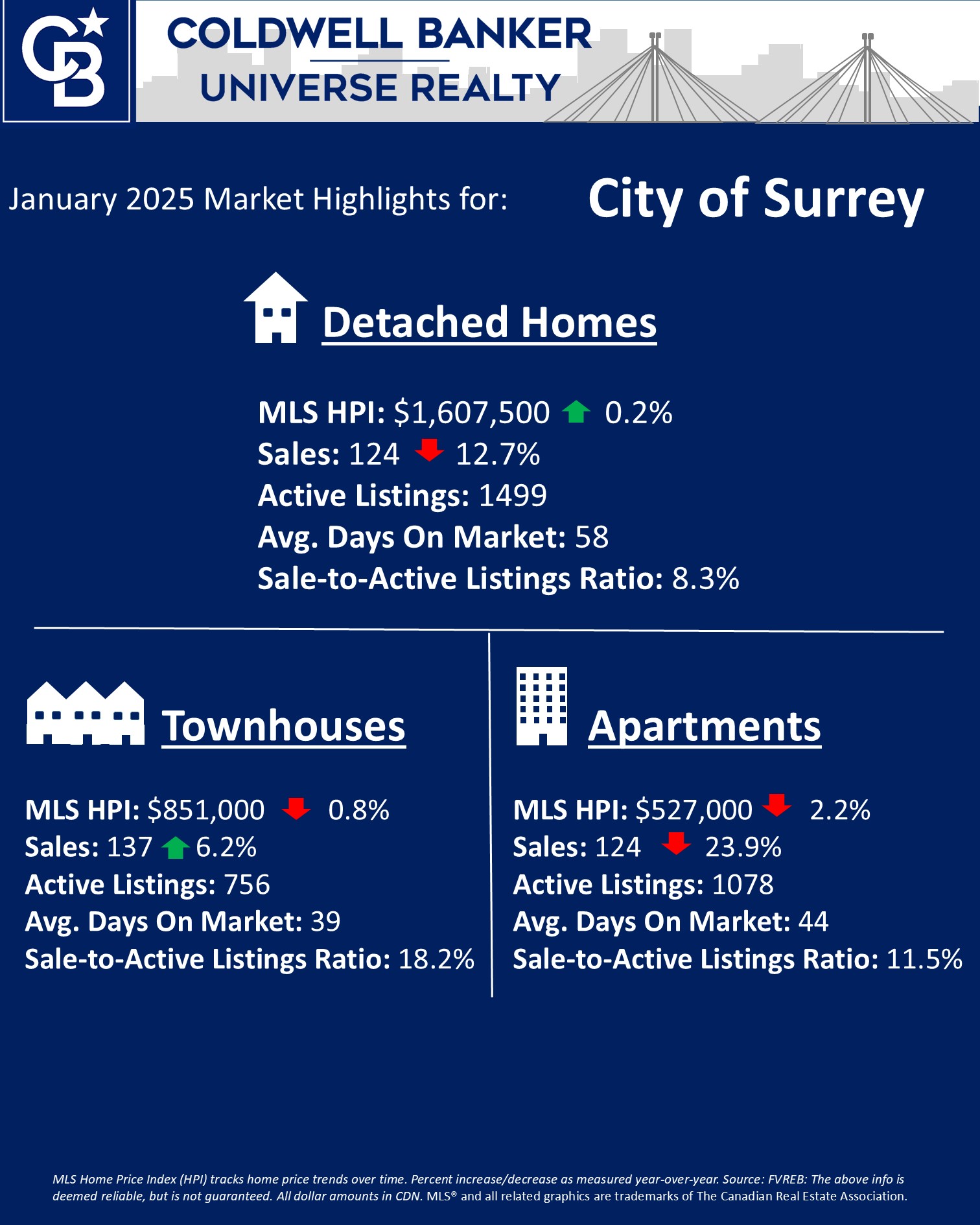

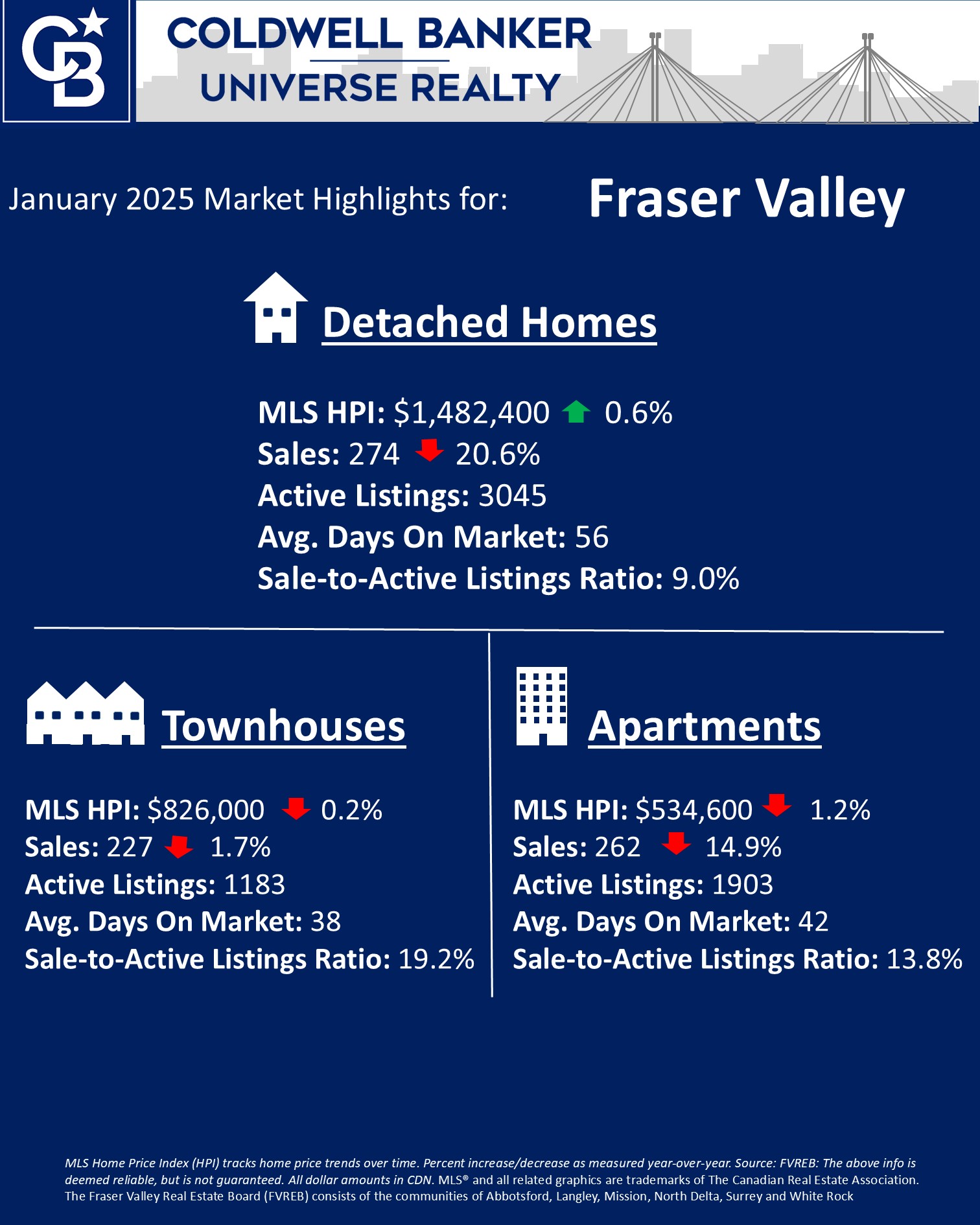

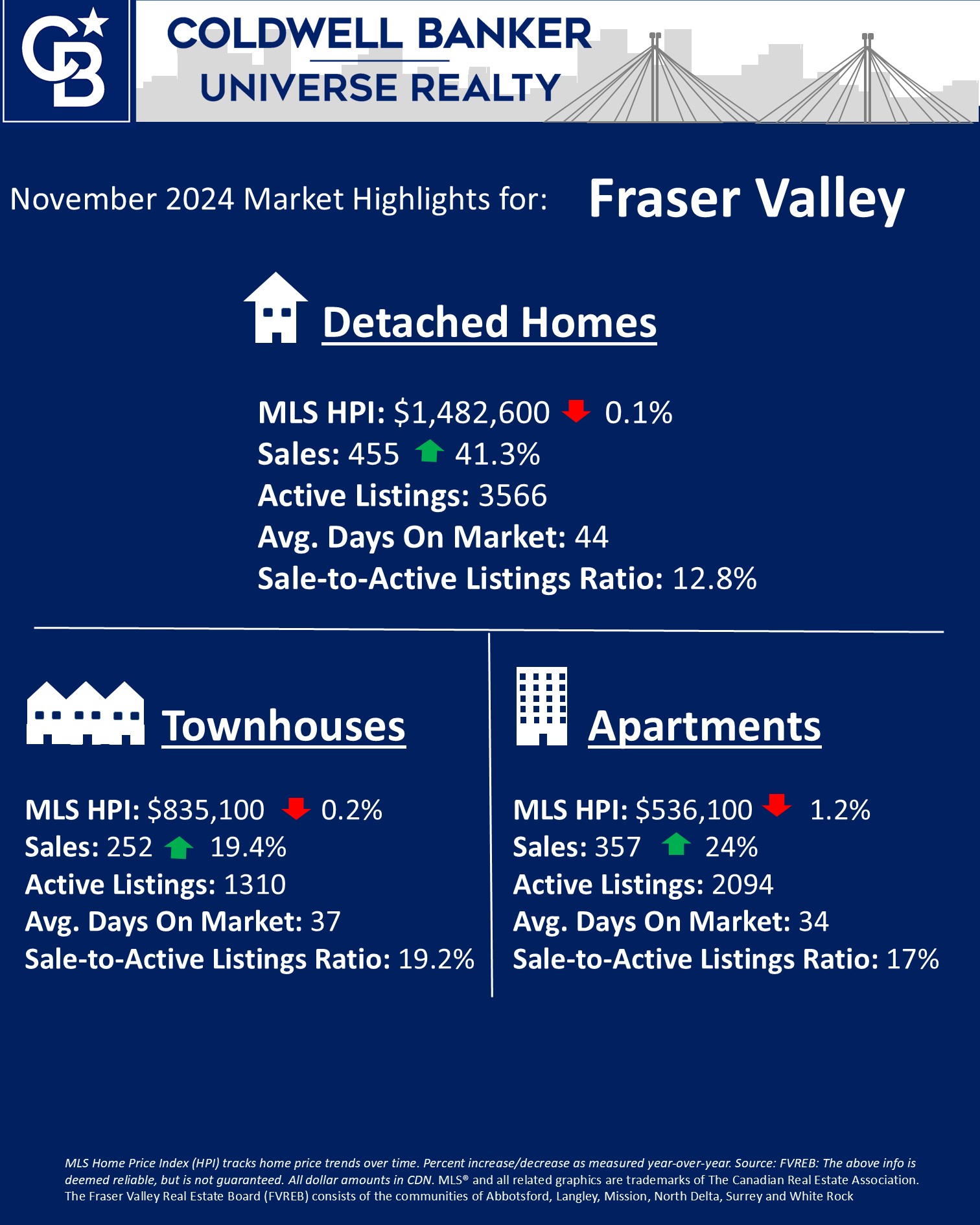

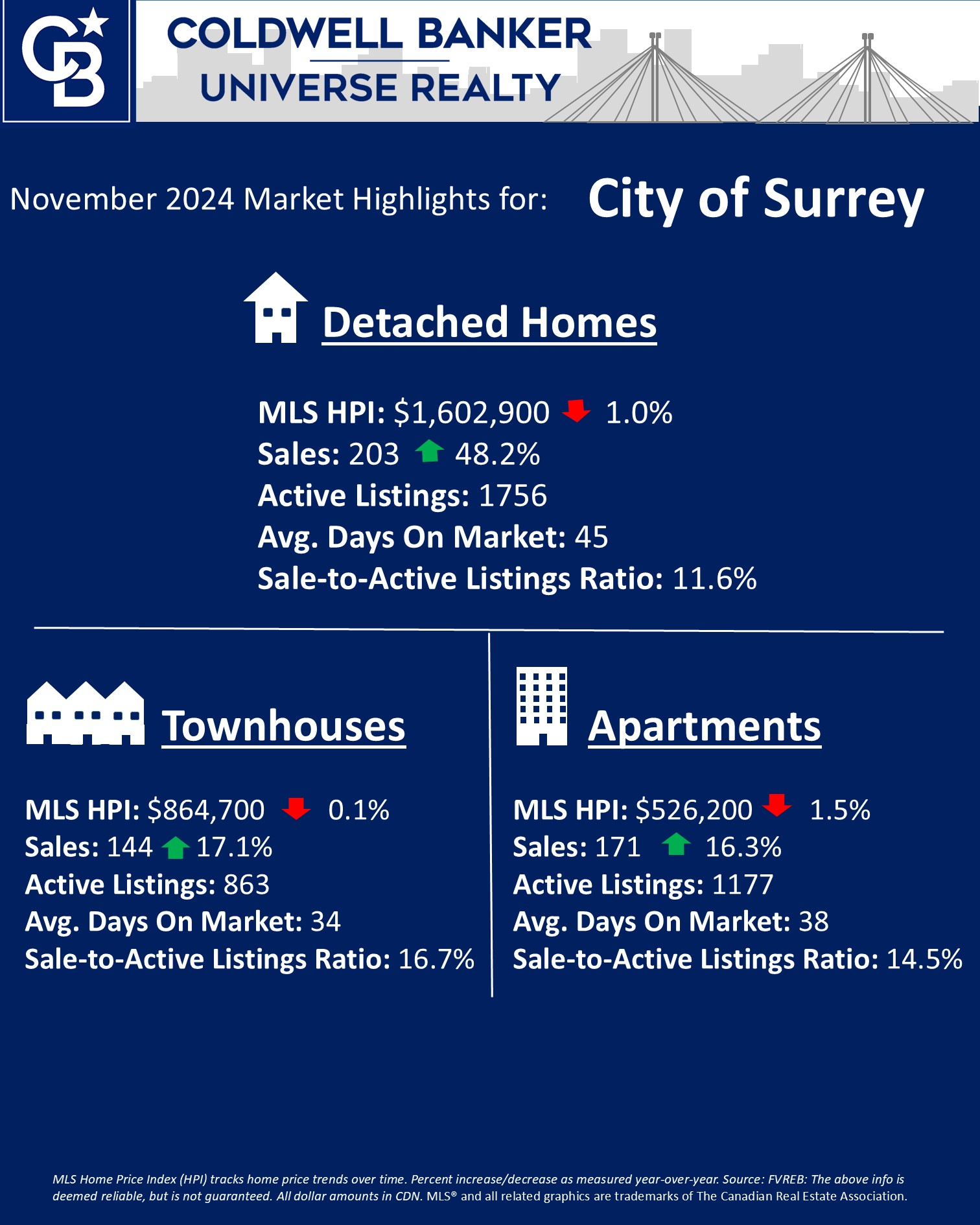

THE MARKET NUMBERS

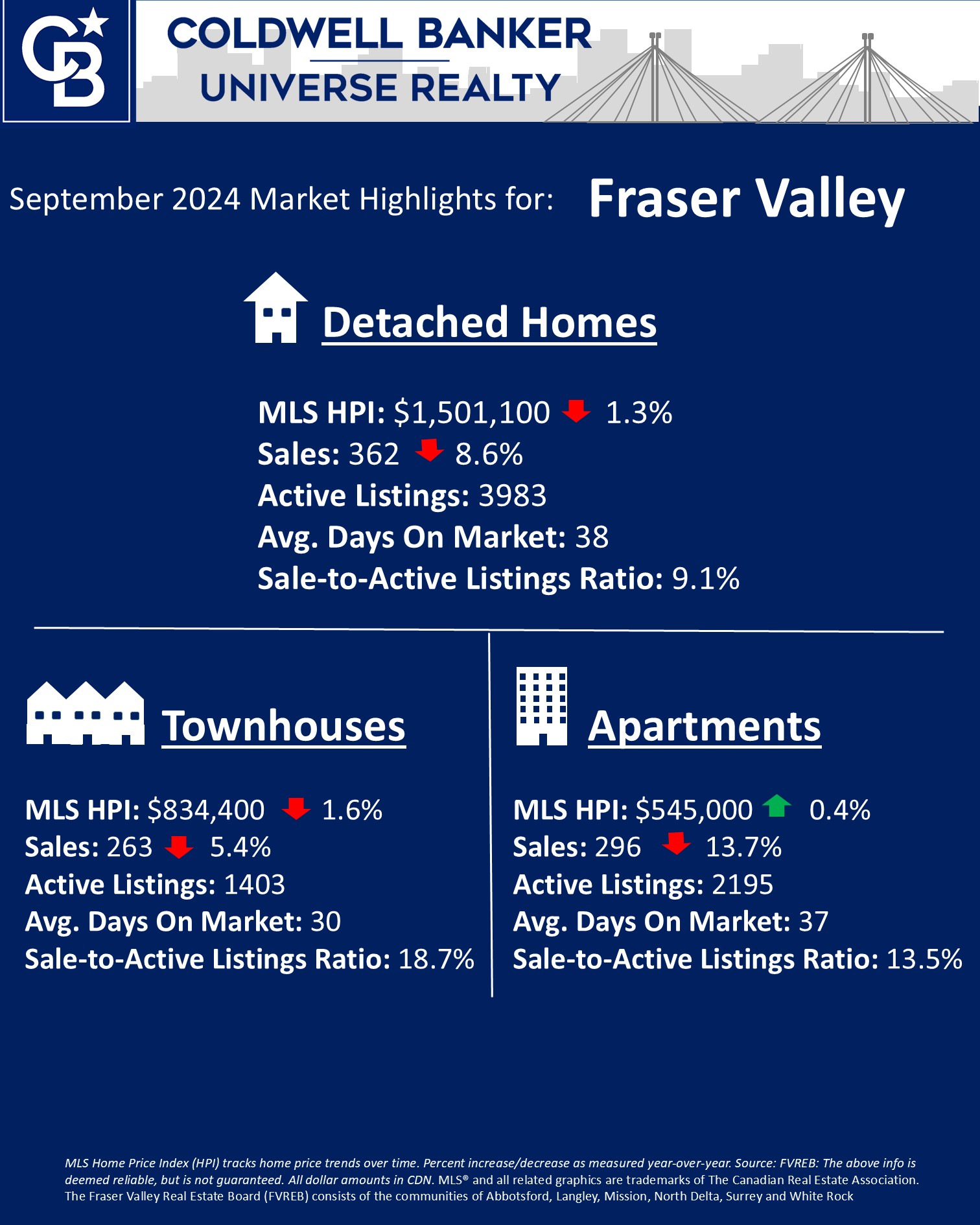

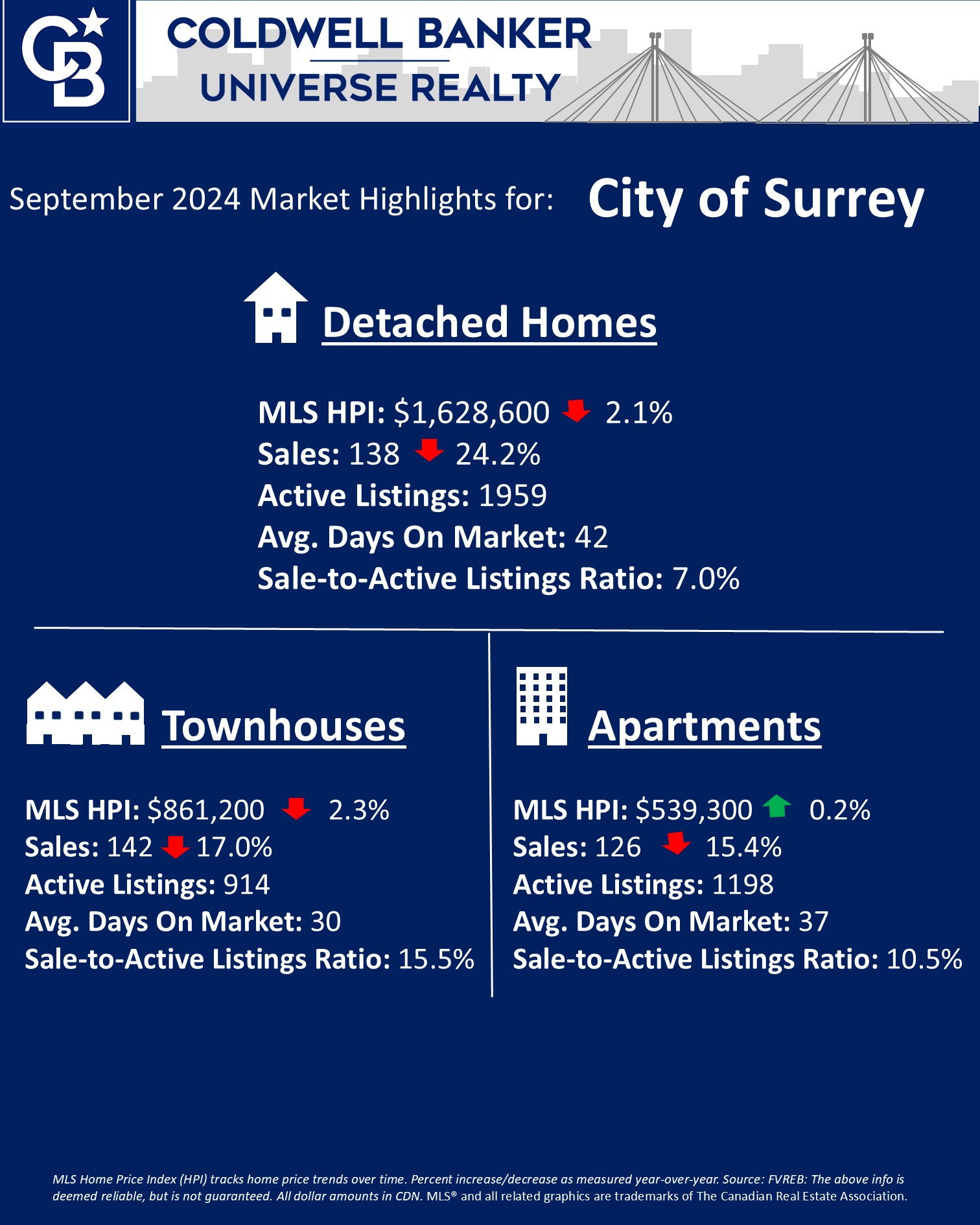

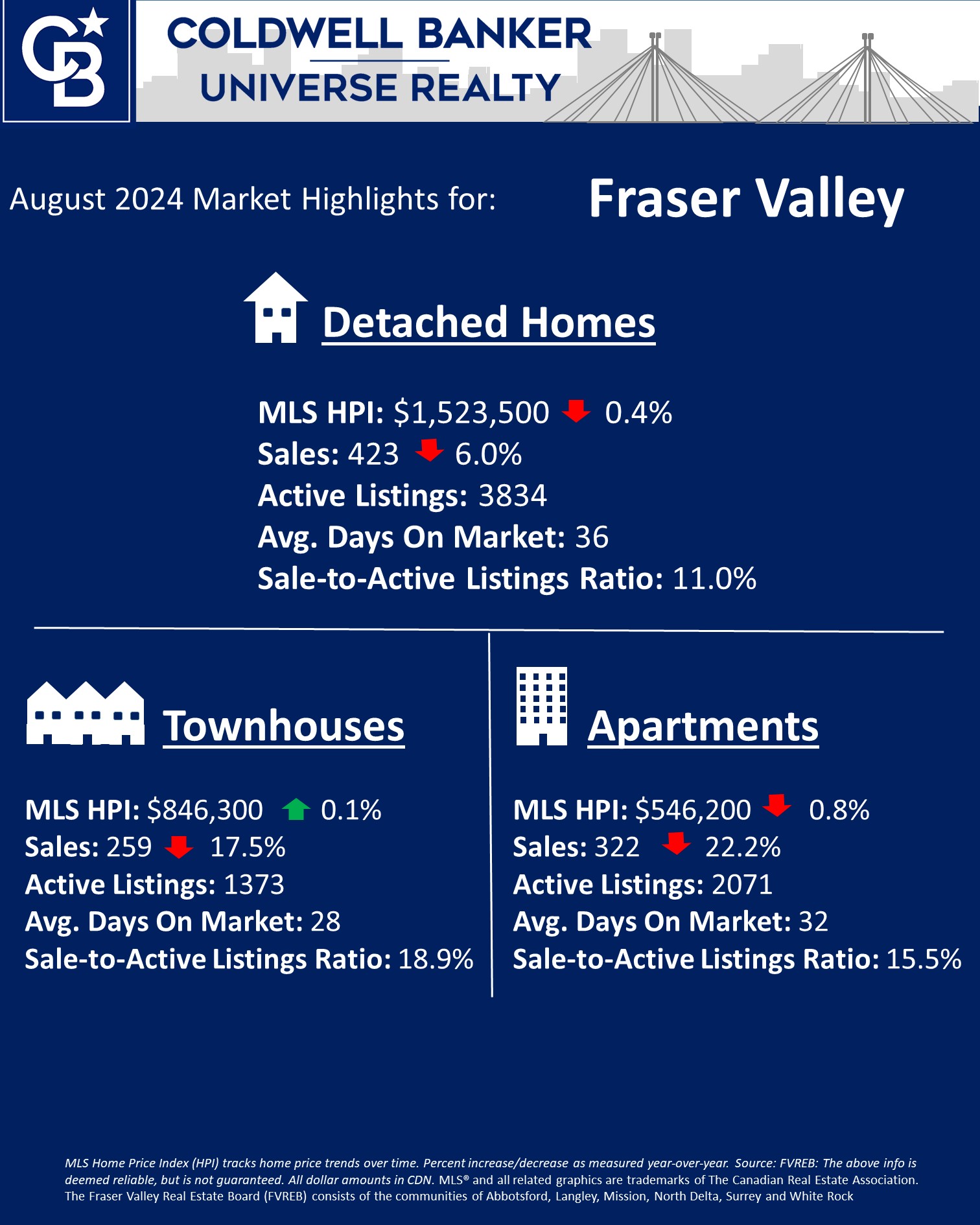

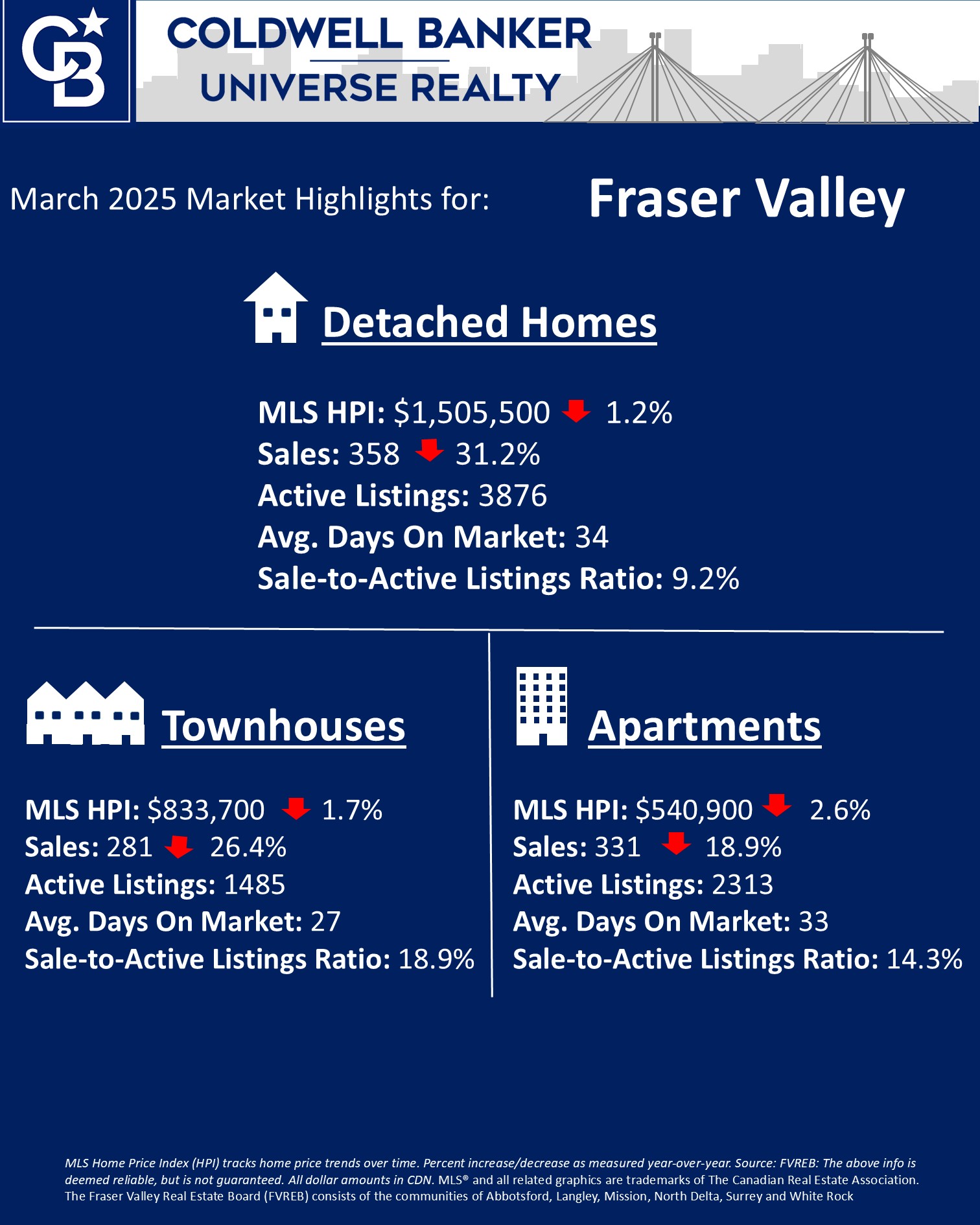

Benchmark prices are slightly lower across the Fraser Valley – down around 3% compared to same time last year.

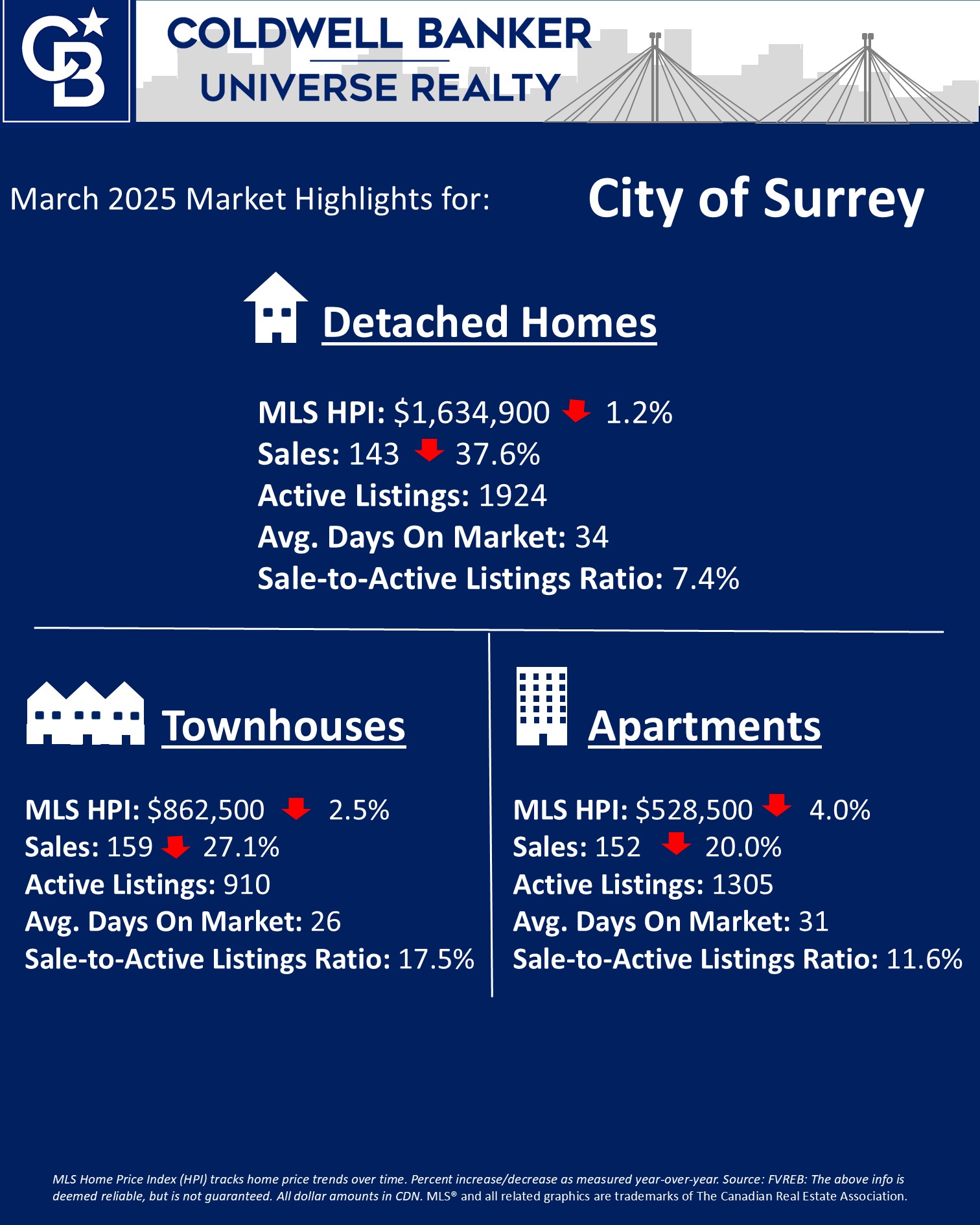

Here are the numbers in the Fraser Valley / City of Surrey:

- Detached = $1,505,500 (-1.2%) / $1,634,900 (-1.2%)

- Townhouses = $833,700 (-1.7%) / $862,500 (-2.5%)

- Apartments = $540,900 (-2.6%) / $528,500 (-4.0%)

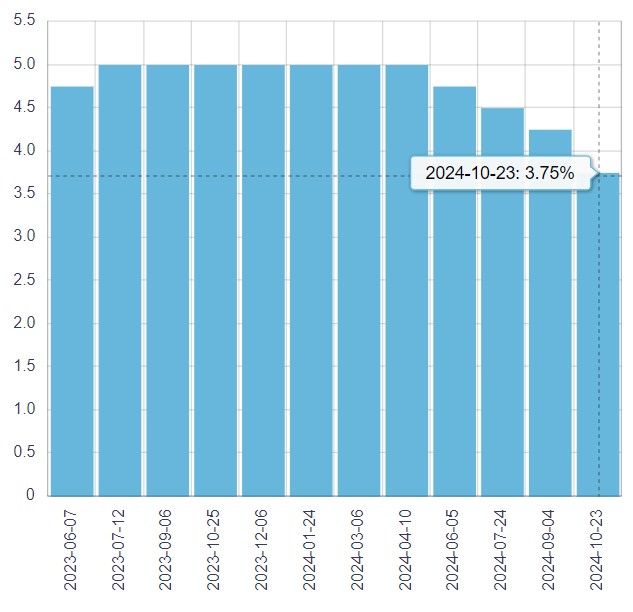

Properties sold a little quicker in March than in February. By property type for the Fraser Valley:

- Detached 34 days in March vs 43 days in February

- Townhouses 27 in March vs 32 days in February

- Apartments 33 in March vs 36 days in February

Overall, the market remains in balanced/neutral territory but detached homes remain in buyer’s territory since the beginning of the year. We recently had the Bank of Canada reduce the policy interest rate FOR THE 7TH TIME! Usually this would spark the real estate market and bring buyers out of the woodwork. But it is clear buyers are taking a cautious approach due to the earlier mentioned market instability.

With higher inventory than we’ve seen in years and with a slower pace of sales due to the uncertainty – the time has never been better… for buyers.

My last bit of feedback for today’s market is simple: A trusted real estate professional can be the biggest asset in your corner.

CONCLUSION

There are always opportunities, even when markets are unsure. While the market is slow, it is still active… and will eventually fully rebound. So if you are curious about what this means for your real estate plans – let’s talk. The time hasn’t been better for buyers in many years but this doesn’t mean rushing out and buying the first thing you see. Work with a professional that can give you up-to-date information, strategies and feedback for today’s market.

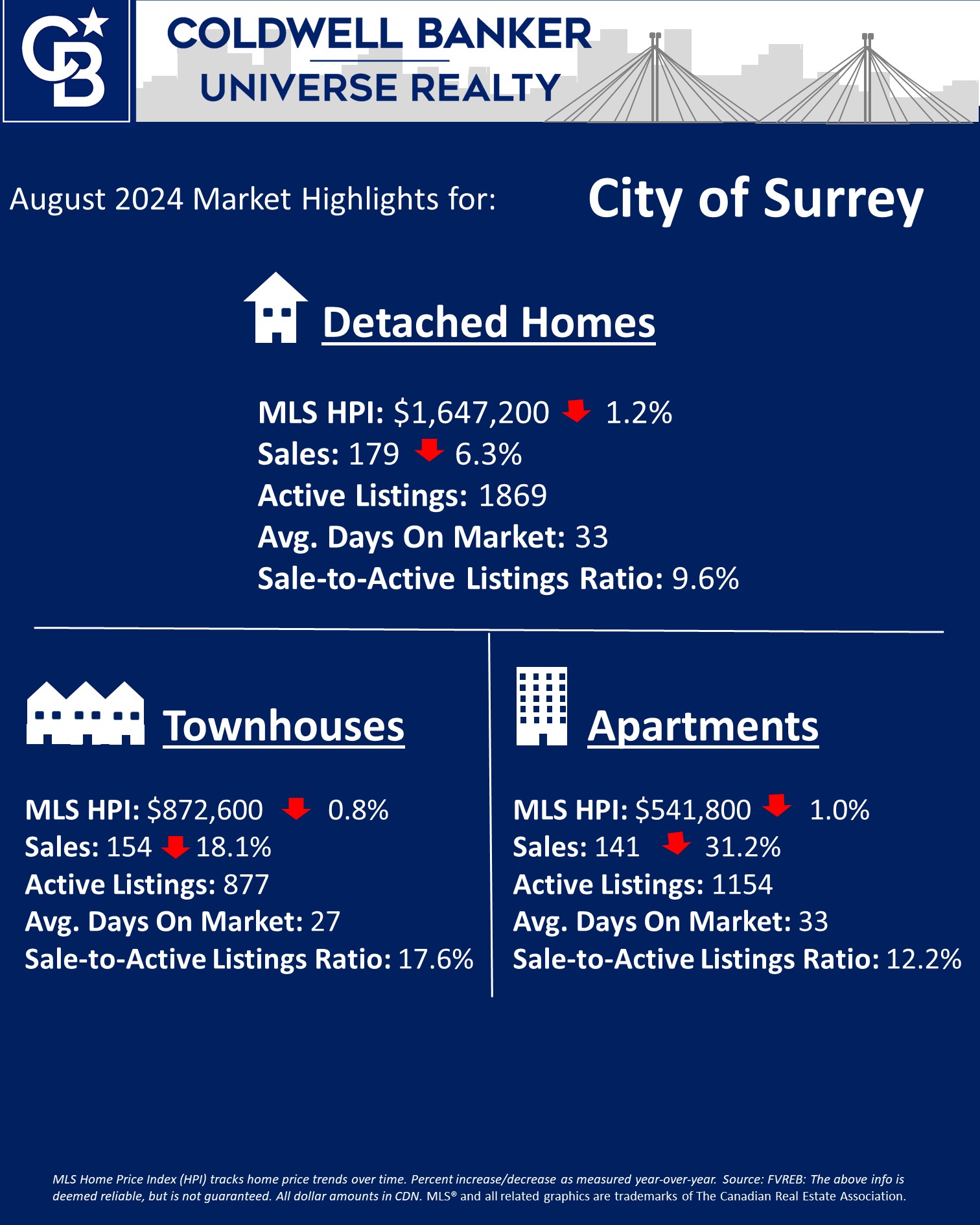

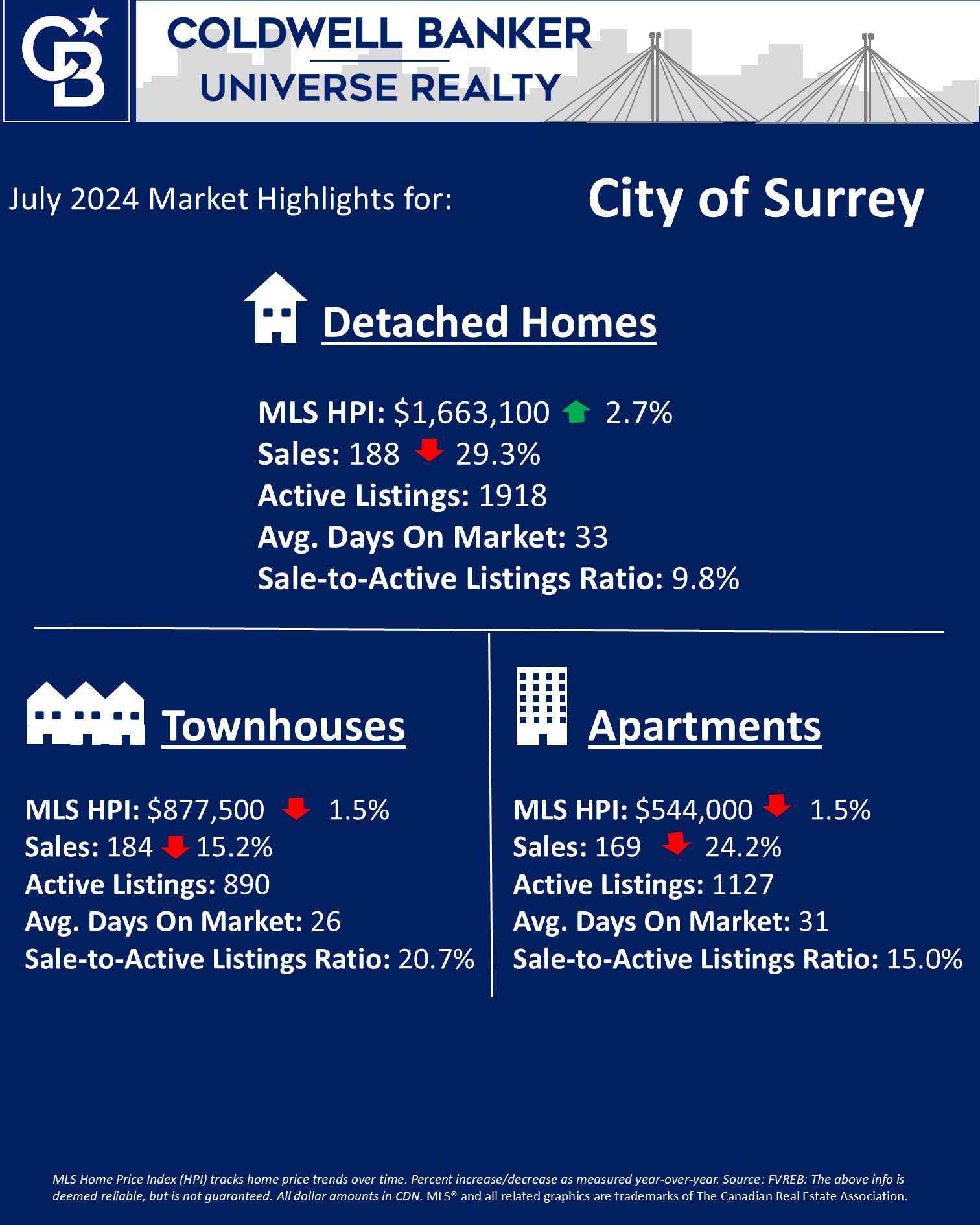

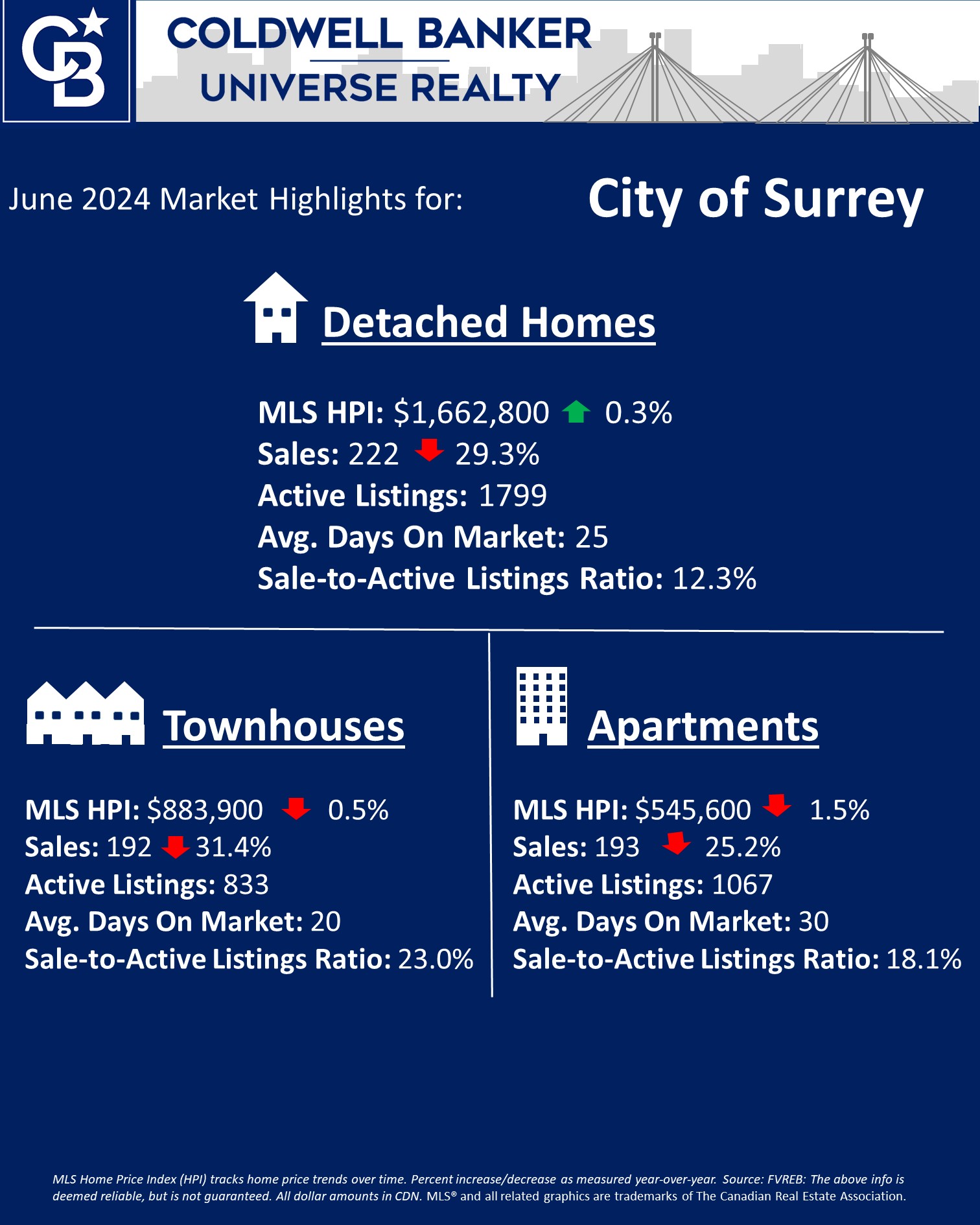

March 2025 Market Update for Surrey

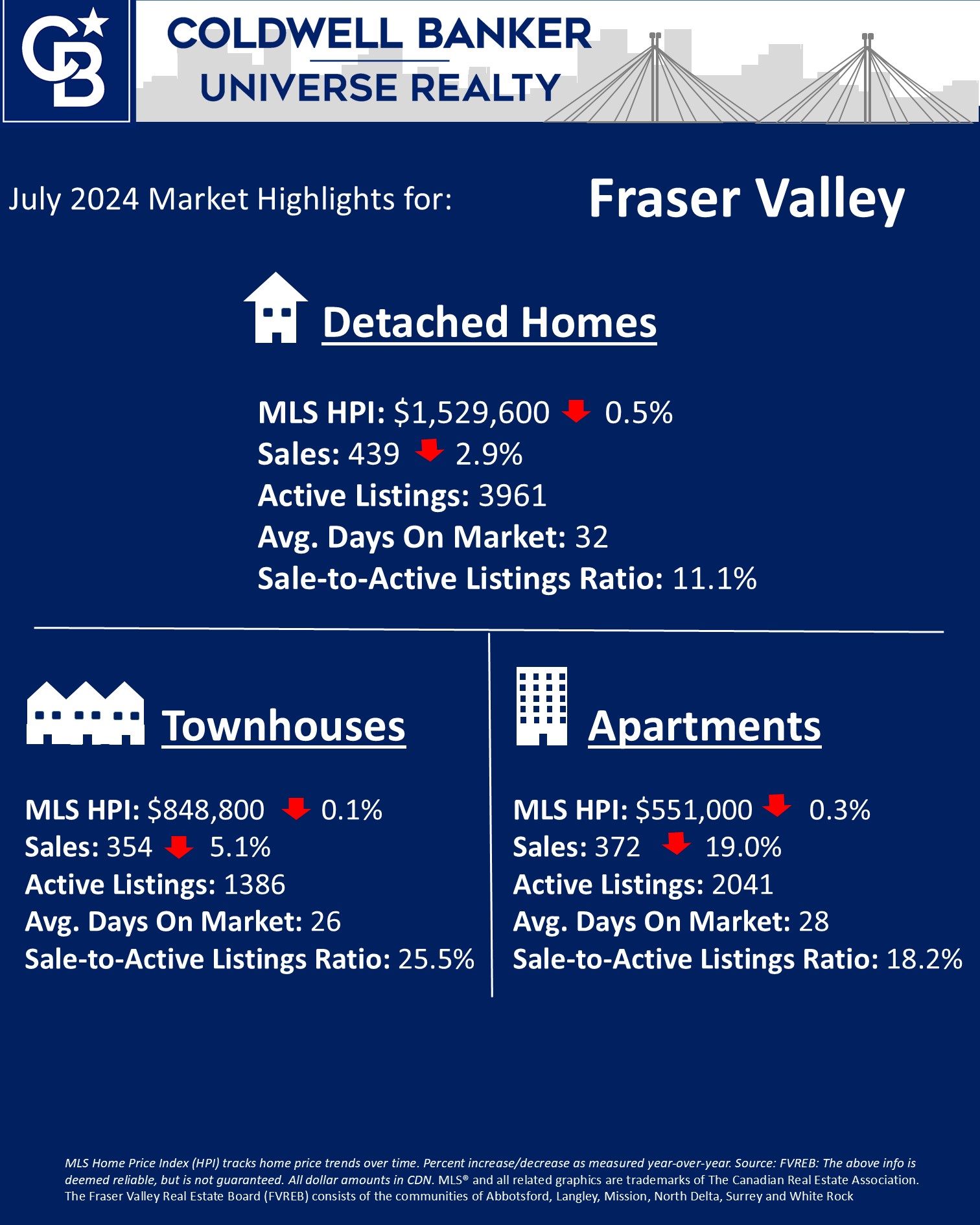

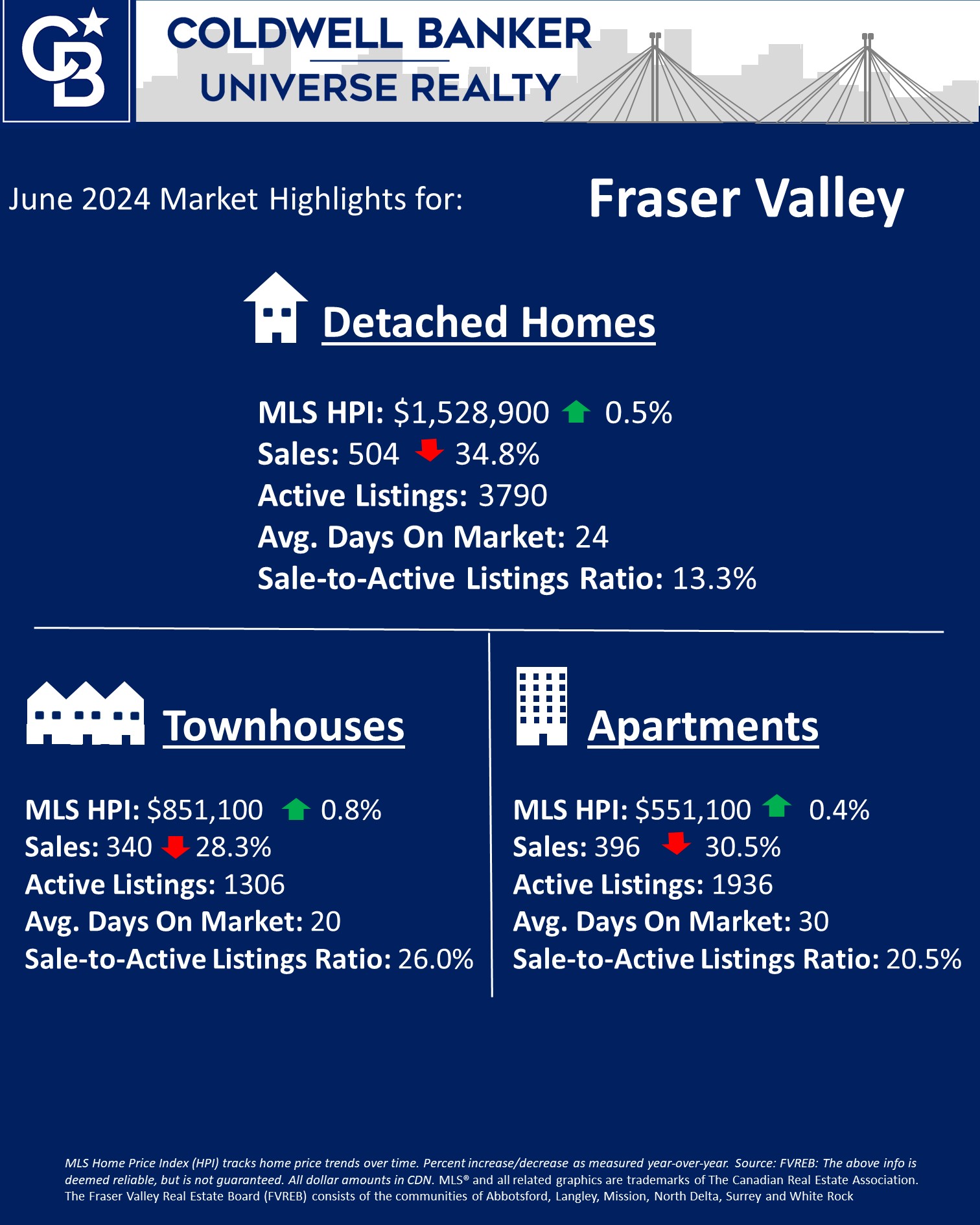

March 2025 Market Update for Fraser Valley

1 – The Fraser Valley Real Estate Board consists of the communities of Abbotsford, Langley, Mission, North Delta, Surrey and White Rock